Housing’s Strength

The housing boom has everything to do with supply and demand, and those fundamental features are not going to change anytime soon.

Doctors, dentists, lawyers, investors, neighbors, family, friends, it seems everybody has an opinion on the direction of housing. Unbelievably, only 19% of consumers believe that now is a good time to buy a home. That means that 81% think it is not a good time to buy. There are TikTok videos proclaiming the inevitable crash in housing. No longer than 3-minutes in length, the clips offer Chicken Little titles with no economic backing whatsoever. From YouTube to Facebook, social media has a big opinion when it comes to real estate. All of the noise, the “Gossip Factory,” feeds on everybody’s collective fears and prevents far too many consumers from making the sound decision to participate in this crazy housing market.

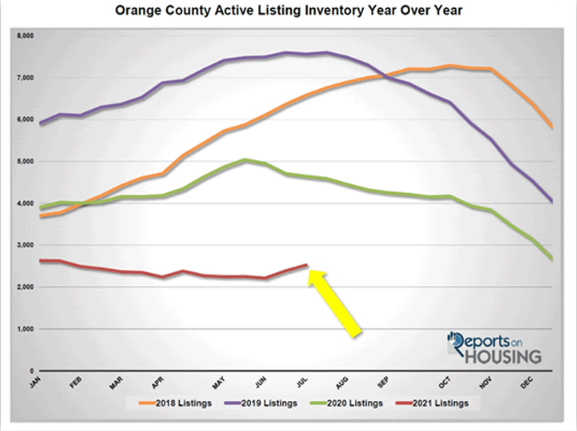

When housing is surging with seemingly no end in sight, society cannot help but flashback to 2001 through 2006. In 2004 and 2005, the Case-Shiller U.S. Home Price Index showed red-hot home price appreciation between 10% and 14.5%. Everybody knows what happened next, the housing bubble eventually popped and led to double digit home price depreciation in 2008 and 2009. In May of this year, U.S. home price appreciation reached 14.6%, its highest level since tracking began in 1988. Yet, today’s housing market is glaringly different than the runup to the Great Recession. That housing stock was built on the backs of easy credit, pick-a-payment plan, subprime lending, zero-down loans, easy qualifying, and fraudulent lending. Prior to the bubble deflating, there were obvious signs of a pending housing collapse: way too much supply of available homes to purchase and diminished year over year demand. The simple Econ 101 principle of supply and demand painted the inevitable housing plunge.

Excerpt taken from an article by Steven Thomas.