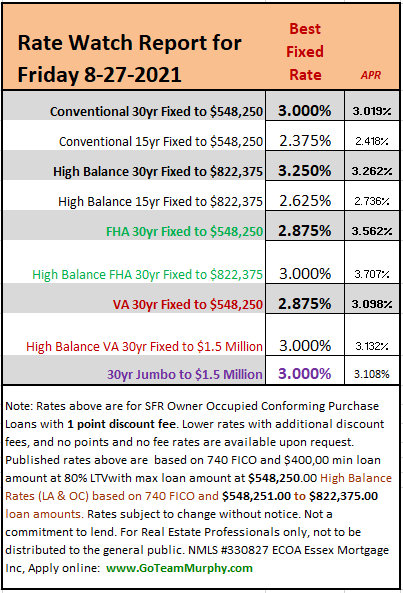

Mortgage Rates have stabilized this morning after moving higher at a moderately quick pace over the past 2 days. To be sure, today’s rates are modestly higher than those seen at the end of last week, despite numerous headlines to the contrary. The headlines in question are based on Freddie Mac’s weekly rate survey which is published on Thursday morning, but tends to capture the “previous” week-over-week rate movement between Monday and the previous Monday.

Why drives mortgage rates though? Rates are dictated by the bond market. As bond prices fall, yields rise, and higher yields coincide with higher rates (indeed, “yield” is simply market jargon for “rate”).

While motivations to buy and sell bonds can vary immensely, the law of supply and demand applies just as it would to almost anything. In other words, if buyers of bonds decide to be less aggressive, bond prices would fall and rates/yields would rise, all other things being equal.

Less aggressive purchase demand is exactly what we’ve seen in the market so far this week. There are at least 2 obvious reasons for this. First, Tue-Thu saw a regularly scheduled round of Treasury auctions. Even though mortgage rates aren’t based directly on Treasuries, they have a strong correlation.

The second reason is a speech from Fed Chair Powell tomorrow. He’s expected to comment on the Fed’s approach to reducing its massive bond buying efforts in the near future (aka “tapering”).

Markets have a pretty good read on Powell’s stance, but there’s a risk that Powell says something that accelerates the perceived time frame for tapering. If that happens, it would imply lower “demand” in the supply/demand equation. In other words, the sooner the Fed tapers, the sooner there is additional downward pressure on bond prices and upward pressure on rates.

If, on the other hand, Powell says the Fed is slowing its roll in response to covid concerns and recently weaker economic data, the buyers who sat on the sidelines so far this week could come back. In that case, rates could recover a bit. Either way, the risk of volatility is increasing. Today just happened to be the day where bonds finally leveled off (perhaps not a coincidence given the end of the Treasury auction cycle and the proximity to the Powell speech).

SOURCE & AUTHOR |

Keith Murphy Branch Manager – Essex Mortgage NMLS #330827

Direct: 714-309-1140

Apply: www.GoTeamMurphy.com