More Choices

While the inventory may still be limited and not even close to returning to pre-pandemic levels, there are finally more homes coming on the market. There are 18% more sellers than last year.

The pandemic severely disrupted the new car supply chain, resulting in inventories hitting an unprecedented low in 2021. New car dealerships looked like empty parking lots. Many interested buyers were forced to pre-order their new automobile purchases. Sales often included a premium and ultimately sold over retail. That all changed as the inventory slowly climbed along with rising interest rates. Finally, there are a lot more cars sitting on the lots. While they have not returned to averages before the pandemic, it is a healthy step in the right direction.

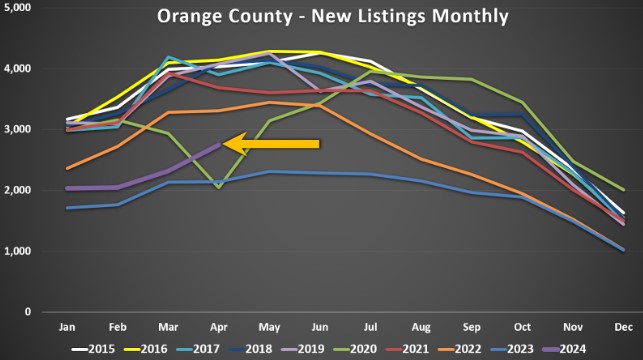

Similarly, housing inventories were severely disrupted during the pandemic. It was not until 2022, when mortgage rates climbed from 3.25% in January to 7.37% in October, that the Orange County inventory finally rose. The supply increased from 1,100 in January until it peaked in August at 4,069 homes, a rise of 269% or 2,969. Yet in 2023, the inventory fell from 2,536 in January to 2,053 in mid-April, a drop of 19%. It then slowly rose until peaking in November at 2,496, an increase of only 22% or 443 homes. Mortgage rates started the year at 6% and eclipsed 8% in October. Affordability was a significant issue, yet the inventory remained relatively flat all year. Intuitively, many thought the inventory would continue to climb rapidly as it did during the second half of 2022 due to the high mortgage rate environment. That was not the case. What happened? Too many homeowners “hunkered down” in their homes and opted not to sell.

Excerpt taken from an article by Steven Thomas.